This week on Tolerable Tax, I want to illustrate the Division 7A (Div 7A) tax consequences of making distributions to Corporate Beneficiaries. If you have a Trust in your operating or investment structure, it is crucial that you have a basic understanding of your Div 7A obligations. For those who’d like to undertake some additional reading on this topic, refer to ATO Tax Ruling TR 2010/3 or ATO Practice Statement PSLA 2010/4 for further information (Hot tip: if you leave a print out of these papers under your pillow at night, the information is taken in by osmosis – its science!).

For context, it is important to understand that the Net Income of a Trust is generally distributed at the end of each financial year, unless the Trustee decides to accumulate the income, in which case the Trustee would be liable for the tax on this income, generally at a rate of 46.5%.

A Trustee may distribute the income to a Corporate Beneficiary, being a company owned by either the individual beneficiaries of the Trust or the Trust itself. A distribution at the end of a financial year will result in an Unpaid Present Entitlement (UPE) due to the Corporate Beneficiary.

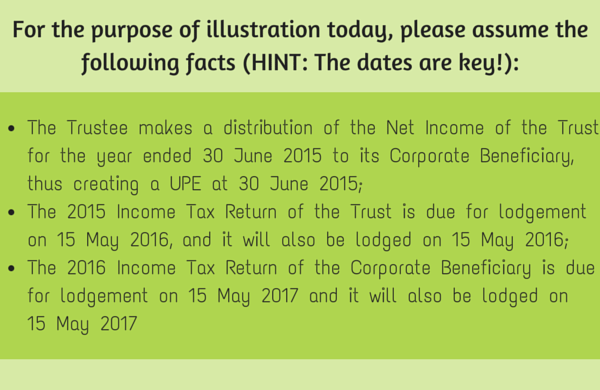

Now, under the requirements of Div 7A, the UPE that arose at 30 June 2015, due by the Trust to the Corporate Beneficiary, must be actioned before 15 May 2016, otherwise it will be considered a “financial accommodation” and become subject to Div 7A.

The actions that may be taken to avoid the UPE being considered a “financial accommodation” are:

1. The Trust can organise for the UPE to be fully paid before 15 May 2016. I would encourage you to consider cash flow requirements, especially if you are operating a business within your Trust;

Note – if you are simply choosing to repay the unpaid present entitlement (and this places a burden on your immediate cash flow), consider extending the period to repay by allowing the unpaid present entitlement to become a “loan” for Division 7A purposes;

2. The Trust can organise for the UPE to put on a sub-trust arrangement as soon as practicable post year end, but before lodgement date of its income tax return.

Note – there are 3 main sub-trust options, a 7 year interest only loan, 10 year interest only loan or specific investment of an income producing asset or investment. Be mindful though, this is only a deferral mechanism; consider deductibility of annual interest and more importantly cash flow planning/forecasting for 7 – 10 years as the principle of the sub-trust will need to be repaid!

If you do nothing before 15 May 2016, the UPE becomes a “financial accommodation”, a fancy way of saying that effectively the Corporate Beneficiary is deemed to have made a “loan” to the Trust on 15 May 2016. From this point in time, you essentially apply the general Div 7A rules to this deemed loan, that is, you have until the lodgement of the Corporate Beneficiary’s Income Tax Return – 15 May 2017 – to ensure appropriate action is taken with respect to the loan, otherwise a deemed unfranked dividend will arise effective 30 June 2016!

Let’s examine the options available to avoid the deemed dividend arising:

1. The Trust can organise for the “loan” to be fully paid before 15 May 2017;

Cash flow planning tip – this effectively gives the Trustee of the Trust 23 months to arrange repayment of the UPE that arose 30 June 2015. This may assist with cash flow planning if you simply wish to repay the UPE and not use sub-trust or Div 7A loan options.

2. The Trust can enter a complying Div 7A loan agreement with the Corporate Beneficiary before

15 May 2017, with the first principle and interest minimum loan repayment being due for payment before 30 June 2017.

Note – again, the use of Div 7A loans is only a deferral mechanism; consider deductibility of annual interest and more importantly cash flow planning/forecasting for the life of the loan as the principle and interest must be repaid!

So, with the above in mind, where to from here?

– Talk to your tax advisors before 30 June 2015 and discuss the use of your Corporate Beneficiary, consider why you are using the Corporate Beneficiary as a vehicle for trust distributions, is there any benefit?

– If there is no longer a benefit to using your Corporate Beneficiary, establish a plan to wind up the company and simplify your Group Structure (saving compliance costs);

– Alternatively, if the Corporate Beneficiary provides a tangible benefit to your operating structure, ensure that you are undertaking cash flow planning to ensure that you are meeting the requirements of Div 7A;

– If you have previously established sub-trust arrangements in prior years, make sure you understand when the principle of the sub-trust (if you used a 7 or 10 year loan) is due for repayment. Consider the cash flow impact on the Trust;

– Finally, if you are simply using the Corporate Beneficiary to defer ”top up” tax on the Net Income of the Trust, it’s well past time to change your thinking! Talk to your tax advisor.

For more information on Div 7a and distributing to corporate trustees, contact DFK Gooding Partners.